- Article

- Macroeconomics, Economic Policy

Crisis Management Plans as Tools for Safeguarding Confidence in Public Finance

February 6, 2020

I would like to consider what macroeconomic policies Japan should pursue for the future. Japan's key policy rate is kept negative, low inflation persists, and public debt stands at more than 240% of gross domestic product (GDP). Given this situation, the goal we should be pursuing at the moment is to direct fiscal resources to income redistribution programs designed to address disparities and the promotion of technological innovation to facilitate growth, based on the prerequisite of avoiding a fiscal crisis (such as an unstable hyperinflation and a sharp rise in interest rates).

Why is this situation, with negative interest rates and low inflation, being sustained? One possible reason is extreme uncertainty. When faced with uncertainty that is so extreme that even the probability distribution is unknown, people feel compelled to prepare for the worst, saving more and spending less. As a result, the natural rate of interest (real interest rate neutral to the economy) turns negative.

There are two broad types of extreme uncertainty that pervade political and economic spheres around the world. One is the growing political instability all over the world, as seen in the rise of populism. One significant reason behind this is growing inequality, a phenomenon that has been progressing globally since the 1980s. Until the 2000s, it had been expected that income inequalities would resolve themselves through the trickle-down effect, but the effect turned out to be insufficient. In fact, inequality is passed from parents to children, dividing societies and destabilizing democracies around the world.

The other type of uncertainty is changes in the defining technologies of industry. Currently, the Fourth Industrial Revolution is underway, with information technology (IT) and artificial intelligence (AI) as its main drivers. While new technologies are full of uncertainty, conventional technologies are becoming increasingly obsolete and investment opportunities are shrinking. The result is extremely high investment demand for safe assets, such as government bonds and currencies, and the emergence of negative interest rates.

The problem of growing inequality should be able to be addressed quickly by implementing income redistribution measures such as reforming the social security system to make it less biased across generations. However, it may take two to three decades to resolve uncertainty arising from changes in the defining technologies. All the while, government bonds will continue to absorb investment demand.

The amount of government bonds outstanding will increase progressively. However, if nominal interest rates (r) on government bonds can be kept at or below zero and the nominal rate of economic growth (g) positive, it is possible to maintain confidence in government bonds so long as uncertainty in the private sector remains high, as explained below. Let's take a look at this scenario.

* * *

Standard economic models assume that an economy eventually converges to a state in which r>g. However, in a 2018 paper, Professor Marcus Hagedorn of the University of Oslo pointed out that it is theoretically possible for an economy to converge toward a long-run state in which r<g. Also, it has been known that r<g as a steady-state condition can be achieved in various overlapping generations (OLG) models and incomplete markets models.

Professor Hagedorn's model assumes that households directly derive utility from holding government bonds. The reason why government bonds bring utility is that government bonds, unlike private-sector assets, have high liquidity and can be used as collateral for financial transactions. Furthermore, the reason why government bonds are highly liquid and collateralizable is high confidence in the government, i.e., the belief that fiscal consolidation will be achieved, under the environment where high uncertainty in the private sector prevails.

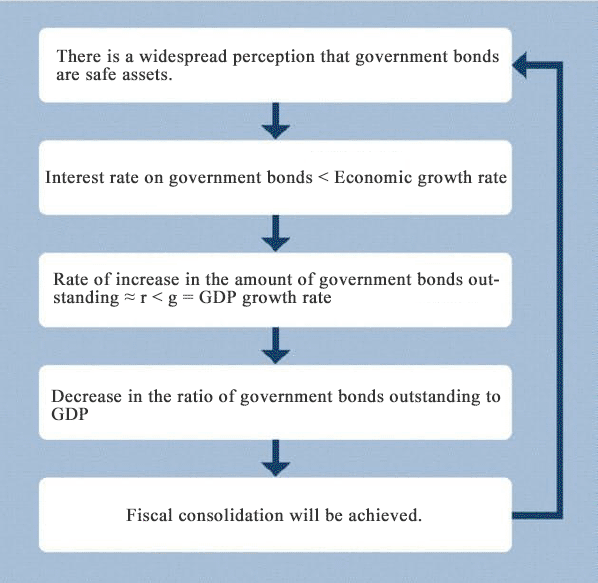

Here, as a scenario to aim for, we can consider the "Good Equilibrium" scenario shown below:

Good Equilibrium Scenario

First, if confidence in public finance—i.e., the expectation of fiscal consolidation—is maintained in the market, government bonds are safe assets. In an economic environment where there is high uncertainty in the private sector, government bonds have higher liquidity and greater value as collateral than private-sector assets. As a result, a state in which r<g can be maintained.

Under this condition, if the government manages to hold down the primary deficit, the government debt ratio—i.e., the ratio of government bonds outstanding to GDP—will gradually decrease and fiscal consolidation will be achieved over an ultra-long-term period, because the amount of government bonds outstanding increases approximately at a rate of r and GDP at a rate of g. Thus, the initial expectation of fiscal consolidation will be self-fulfilling.

At present, it appears that we are unwittingly beginning to follow the Good Equilibrium scenario. In this case, the government will not have to implement tax increases and other austerity measures at a pace or to a degree that is excessively severe, and there will be leeway to make necessary expenditures in a way that is to some extent well balanced, for instance, to enhance the social security system to make it less biased across generations. In order to enable this, the government needs to implement the following two policies.

The first policy calls for reducing the primary deficit. More precisely, it calls for realizing a situation in which the government's deficit does not continue to increase. If the amount of deficit remains a finite value, the government debt ratio converges to a certain value when r<g, and the fiscal situation will stabilize. The conditions needed to achieve r<g in the Japanese economy are that the expectation of fiscal consolidation is shared widely in the market and that an extremely high level of uncertainty in the private sector continues. If these conditions fail to hold, interest rates will begin to rise, and the economy will enter a state in which r>g.

Preparing for this possibility is the second policy, which involves developing a crisis management plan. Interest rates can go up in various ways. If interest rates rise as uncertainty in the private sector disappears and private-sector investment is activated, the economy will become overheated and tax revenue will increase, making it politically easier to raise taxes and cut spending. Also, if higher interest rates are the result of upward pressure brought about by overseas factors (conflict, economic crisis, etc.), we will see a similar situation to the case of higher interest rates resulting from expanded investment, in response to the possibility that the yen will depreciate and the economy will expand.

* * *

However, if a loss of confidence in public finance triggers capital flight from Japanese government bonds (JGBs) and the yen to the U.S. dollar and other assets, it will put enormous upward pressure on interest rates. If the Bank of Japan (BOJ) expands the money supply by purchasing JGBs indefinitely in order to suppress the rise of interest rates, inflation will become uncontrollable, creating a fiscal crisis.

Therefore, in order to safeguard confidence in public finance, it is imperative to develop, during normal, or non-crisis periods, a crisis management plan that can assure the market of the government's ability to resolve such a crisis. As emergency measures to combat a crisis, such as massive selloffs of JGBs, a scheme should be developed to enable the BOJ to stabilize the JGB market, and triage procedures should be established for selectively suspending the execution of budgets. Also, long-term measures for improving fiscal balance should be described in specific detail.

Some studies have shown that the fiscal balance must be improved by 14% of GDP (approximately 70 trillion yen), which will require drastic reform. Despite preparing a plan for such reform, Japan should aim to realize the Good Equilibrium scenario in which the plan will not need to be executed. Until now, government officials have been worried that if they develop a crisis management plan, the news would upset the market and could trigger a fiscal crisis. Thus, just discussing such a plan publicly has been considered taboo.

However, in the current situation where r<g, there is no need to be overly sensitive. There is an expectation that the amount of government bonds outstanding will gradually decrease, and we are not in a situation where uncertainty could trigger a crisis. In the past, it was argued that government intervention in solving the problem of bad loans would spur a crisis. However, as it turned out, when the government stepped in, the market stabilized. We must take heart from that experience.

Reprinted with permission from the website of the Research Institute of Economy, Trade, and Industry. Translated by RIETI from “Zaisei shinnin e ‘kiki taio pruan," Keizai Kyoshitsu, Nihon Keizai Shimbun, October 16, 2019.

-

-

- RESEARCH DIRECTOR

- Keiichiro Kobayashi

- Keiichiro Kobayashi

- Areas of Expertise

-

- Macroeconomics

- financial crises

- economic philosophy

- Research Program

-

- Quantitative Analysis of Epidemics and Economic Implications ( –2023)

- Future Design: Research on Decision-Making Methods for Intergenerational Sustainability ( –2021)

- Plans for Sustainable and Politically Acceptable Fiscal Consolidation and Social Insurance Reform from the Perspectives of Behavioral Economics and Political Science(-2024)

- Economic Analyses of Pandemics

-

Featured Content

-

Funding the Policies to Boost Japan’s Birthrate

Funding the Policies to Boost Japan’s Birthrate

-

CSR in Japan: Unique Features and Recent Trends

CSR in Japan: Unique Features and Recent Trends

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

-

Is the Digital Transformation of Education a Realistic, Sensible Goal?

Is the Digital Transformation of Education a Realistic, Sensible Goal?

-

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform