- Article

- Industry, Business, Technology

TCFD-Recommended Climate Related Information Disclosure and Business Strategy in Times of Uncertainty

May 24, 2021

Embracing the TCFD Recommendations would not only help businesses maintain their corporate value in the face of growing uncertainty but also ensure the flow of capital to truly resilient companies, resulting in a healthier financial system.

* * *

There is growing awareness in Japan and around the world of the impact climate change can have on corporate value. Terms like climate-related financial disclosures are cropping up lately in conversations among businesspeople, and news of natural disasters often refer to the damage companies incur to their market value. In the following I will examine the broadening links between climate change and corporate value, outline the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD) and the benefits conformance can confer, and discuss ways to build a more resilient management strategy for an era of heightened uncertainty.

What Are the TCFD Recommendations?

In December 2015, the Group of 20 requested the Financial Stability Board to assess the impact of climate change on the financial sector. It was out of this assessment that the board created the TCFD. This was the same month that the Paris Agreement was adopted by 196 state parties at the UN climate change conference in France with the goal of limiting global warming in 2100 to below 2 degrees Celsius compared to pre-industrial levels. The TCFD’s mandate was to develop a framework for more effective climate-related disclosures that could promote informed investment, credit, and insurance underwriting decisions and, in turn, enable stakeholders to understand better the concentrations of carbon-related assets in the financial sector and the financial system’s exposures to climate-related risks.

The task force is chaired by former New York Mayor Michael Bloomberg, under whose leadership a final report titled the Recommendations of the Task Force on Climate-related Financial Disclosures was issued in June 2017. The report, commonly referred to simply as the TCFD Recommendations, contains a framework enabling companies in any industry to disclose their climate-related risks and opportunities. The recommendations are not legally binding, and businesses can choose to follow them at their own discretion.

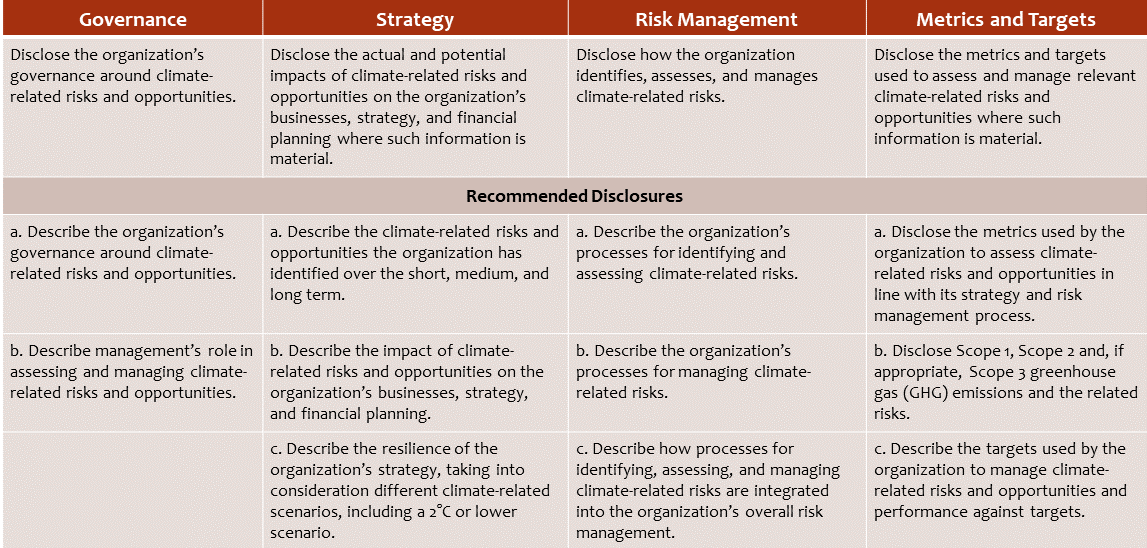

The recommendations call for disclosures in four thematic areas representing core elements of how organizations operate: governance, strategy, risk management, and metrics and targets. They also cite 11 “recommended disclosures” within those four areas (see Figure 1). In the context of TCFD-recommended disclosure, climate-related risks are divided into two major categories: (1) risks related to the transition to a lower-carbon economy and (2) risks related to the physical impacts of climate change. The former refers to the extensive mitigation requirements related to climate change, such as the introduction of new policies and regulatory mechanisms, technological improvements or innovations, market shifts in supply and demand, and reputational risk tied to shifting customer or community perceptions. The latter includes the increased severity of extreme weather events induced by higher global temperatures, such as typhoons, torrential rainfall, droughts, and rising sea levels. These may also result in the loss of ecosystems and reductions in farm production or fisheries catches. As for opportunities, the recommendations cite enhanced resource efficiency, higher investments in renewable energy capacity, the development of innovative products and services, and access to new markets by capitalizing on shifting consumer preferences.

The significance of the TCFD Recommendations lies in its endorsement of treating climate-related risks and opportunities as financial information and conducting scenario analysis to assess the impact of such risks and opportunities on corporate operations. Previously, information about the “E” in ESG (environmental, social, and governance) management was commonly described in qualitative terms and outlined in nonfinancial reports. The recommendations thus represent a big step forward in creating a framework for the quantitative disclosure of ESG data.

Figure 1. The TCFD Recommendations on Climate-related Financial Disclosures

Source: Final Report: Recommendations of the Task Force on Climate-related Financial Disclosures, 2017.

In concrete terms, this means publishing the findings of an analysis of how climate-related risks and opportunities could impact on corporate income statements and balance sheets. Under the scenario where the world transitions to a lower-carbon economy, for example, a company would need to calculate the expected rise in energy costs when a carbon tax is introduced. For many businesses, quantitatively ascertaining and assessing climate-related risks and opportunities will be a new challenge, since few have taken the trouble to conduct such analyses prior to the publications of the TCFD Recommendations.

The Impetus for Climate-Related Disclosures

Climate Change as a Global Risk

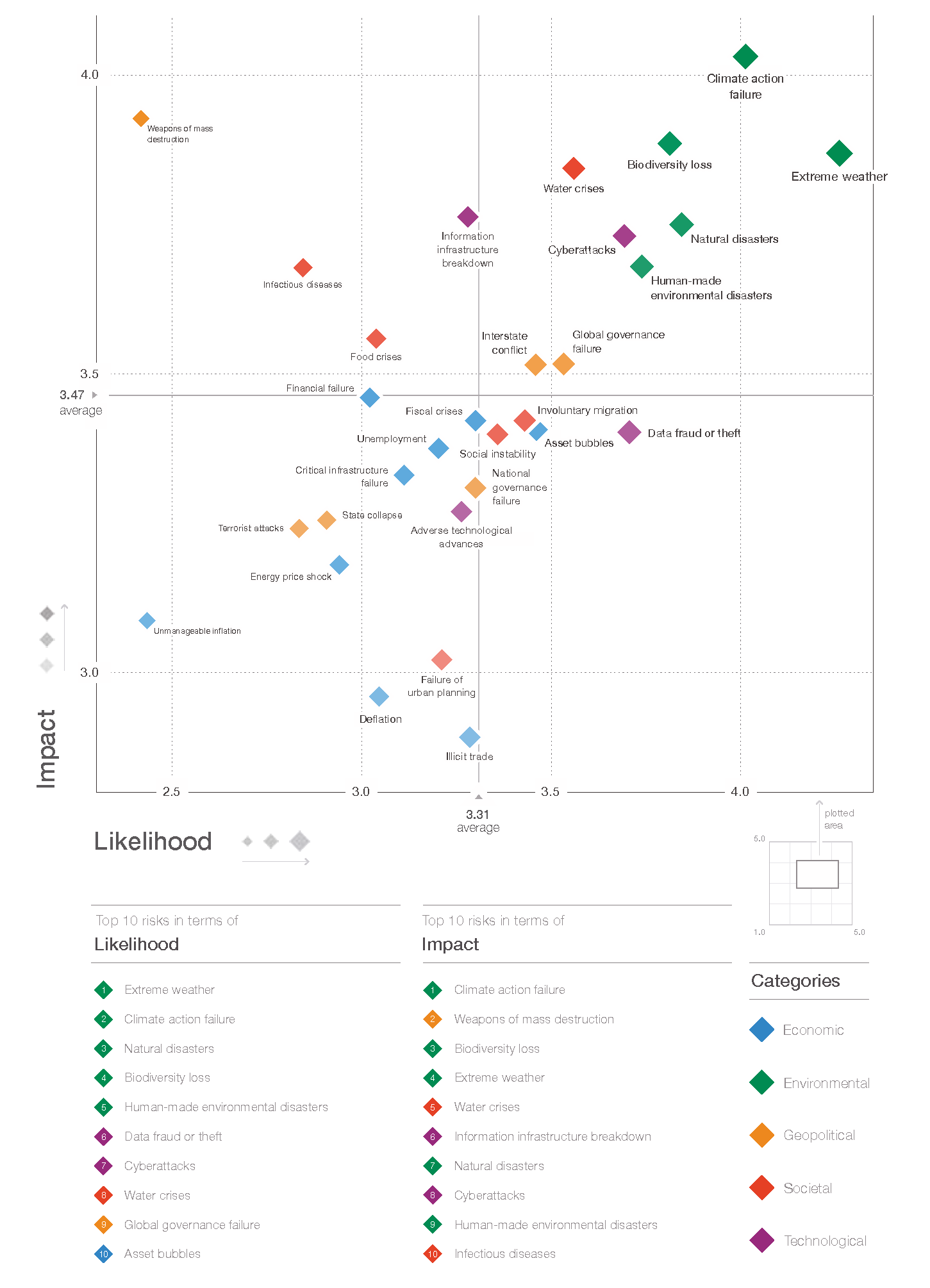

Each year, the World Economic Forum issues a Global Risks Report outlining the biggest risks in terms of likelihood and impact. The report incorporates information and opinion not just from industry but also from government and academia and offers a glimpse into what the world perceives to be the greatest threats. The 2020 report, incidentally, was the first in which all top five risks were in the environmental category—namely, (1) extreme weather, (2) climate action failure, (3) natural disasters, (4) biodiversity loss, and (5) human-made environmental disasters—with the top four being climate-related (Figure 2). A glance at the risks landscape between 2007 and 2020 indicates, moreover, that the seriousness of environmental risks (green-shaded cells in Figure 3) has been steadily growing over the past 14 years.

Figure 2. The Global Risks Landscape 2020

Source: World Economic Forum, Global Risks Report 2020.

Figure 3. The Evolving Risks Landscape, 2007–2020

Source: World Economic Forum, Global Risks Report 2020.

Infectious diseases, incidentally, are included in the Global Risks Landscape (Figure 2) as one of the top 10 risks in terms of impact. Infectious disease experts have long pointed to the dangers of a pandemic, so presumably not all global business leaders were caught off-guard by the outbreak of COVID-19, but at the same time, I doubt many had taken the step of quantitatively analyzing the impact of such a crisis and had a grasp of its financial consequences.

The task force’s recommendation that businesses quantify climate-related risks and analyze their financial impact is intended exactly to circumvent the kind of global economic dysfunction and financial market disruption that we are seeing today. It is also aligned with the maxim, often attributed to management guru Peter Drucker, that “you can’t manage what you don’t measure.”

Disclosing the Value of Intangible Assets

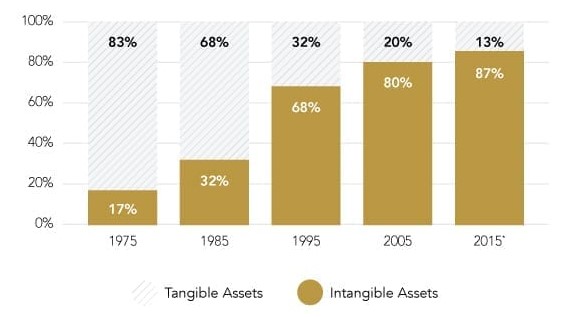

Financial data is indispensable when assessing the value of publicly listed companies, but such information alone is no longer enough to ensure a proper market value. This is because corporate value is now largely derived from intangible assets, which are difficult to ascertain just by looking at financial statements. Figure 4 shows, in fact, that close to 90% of the market value of US traded companies comes from intangible assets. The five global tech giants—Google, Amazon, Facebook, Apple, and Microsoft—were together worth US$64 trillion as of July 2020, and Apple alone was valued at over $20 trillion the following month, exceeding the market cap of Saudi Aramco. The large number of e-commerce clients and social media members as well as many streaming and gaming platforms are examples of intangible assets that are the chief source of wealth, though their market value cannot be readily ascertained.

Figure 4. Components of S&P 500 Market Value

Source: Ocean Tomo website.

GAFAM are not the only ones whose key assets are intangible; the primary sources of long-term corporate value for most other firms, too, consist of such intangible strengths as the capacity or technology to spawn innovation, human resources and organizational culture, and management skills, including those to navigate crises. Yet there is no reliable way of measuring such assets or comparing them with what other companies possess. This indicates that capital—the life blood of the economy—may not be flowing to the right places (companies), resulting in a disconnection of the “investment chain.”

The TCFD Recommendations were designed to rectify such a disconnect that had existed in corporate disclosures of climate-related information. They call on companies to describe the resilience of their strategies under different climate-related scenarios, such as one in which the current reliance of fossil fuels continues and another where the world transitions to a lower-carbon economy. The former could lead, beyond 2030, to severe natural disasters that devastate the ecosystem, while the latter would mean tighter regulations on greenhouse gas emissions requiring innovative new technologies and responses to shifting market needs. Financial disclosures in line with the recommendations would enable investors to identify and channel funds to the most resilient companies and thereby ensure financial market stability.

The Benefits Outweigh the Costs

In order to make climate-related disclosures, companies must first undertake a business impact analysis and institute in-house changes affecting all relevant sections. This may incur costs in terms of time and personnel, and senior management may wonder whether such costs are worth the effort. After all, there will be no imminent downsides to not making such disclosures; share prices are not going to suddenly plummet due to a negative market assessment. But senior management should note that the number of institutional investors embracing ESG principles has been rising steadily, and the value of ESG investments is growing year by year. In his 2020 letter to CEOs, BlackRock CEO Larry Fink talked at length about climate change, emphasizing that “Climate risk is investment risk” and noting that the “TCFD provides a valuable framework” for “evaluating and reporting climate-related risks, as well as the related governance issues that are essential to managing them.”

In August 2019, Japan’s Government Pension Investment Fund published the findings of a climate-change analysis of its investment portfolio. The GPIF conducted a scenario analysis in 2020 and disclosed an assessment of climate-related transition and physical risks. Such steps by the world’s largest public pension fund are likely to spur additional climate-related assessments by asset managers in Japan.

Companies, especially those that are publicly traded, can thus expect to face increasing risks and costs if they do not disclose climate-related data. If such information is not forthcoming from the company itself, investors will look for it elsewhere, even if the reliability of third-party sources is suspect. Businesses must realize that in the digital age, they are ultimately responsible for any misperceptions that could arise from a failure to properly disclose their sustainability-related information. They need to communicate information about themselves proactively and correctly to their stakeholders to ensure a proper assessment of their market worth.

Climate-related disclosures are important for both companies and investors, as Larry Fink notes, but assessing the potential impact of climate change and making strategic decisions about how to respond are fundamentally more critical for the company. Many businesses could be forced to overhaul their management strategies or even their business models should there be a need to shift energy sources or secure natural resources vital for businesses, precipitating tectonic changes in the very structure of the economy. At the very least, they would need to revise their medium-term business plans as they invest in energy-saving production equipment and transport systems and seek out new, stable means of material sourcing. This is a task that is likely to take not months but years as they take stock of their strategic options and formulate new business plans.

The process of self-inspection is crucial even in sectors of the economy that are not projected to be adversely affected by climate change. Companies need to reflect on the resilience of their vision for long-term growth, on which their current management strategies and medium-term business plans are based. Given the difficulty of managing what one cannot measure, the very effort to quantify various climate-related risks and opportunities can generate insights quite distinct from those gleaned just through qualitative analysis. The assigning of monetary values will give companies a clearer image of how they may be impacted and allow them to compare the range of scenarios. Conducting quantitative analysis will mean more work, to be sure, but the benefits are well worth the costs.

Learning from the Future

From the viewpoint of management strategy, the biggest challenge climate change poses going forward will be coping with uncertainty. Most businesses were unprepared for the economic havoc caused by the outbreak of COVID-19. Having now been made acutely aware of how uncertain the future can be, they can no longer afford to regard the pandemic and other risks as externalities. Corporate value will henceforth accrue from how well companies manage unforeseen eventualities.

Many companies today rely on past data and heuristics to draft their growth strategies. But in an increasingly uncertain and unpredictable world, developing strategies by looking at the past is no longer enough; what is needed is a method of “learning from the future.” Scenario analysis, the TCFD notes, represents such a tool. Originally developed by the RAND Corporation for the US armed forces to formulate defense strategies in the era of great uncertainty following World War II, scenario planning was famously utilized by Pierre Wack at Royal Dutch Shell, who learned from Herman Kahn of the RAND Corporation to minimize the impact of the oil crises in the 1970s, enabling Shell to ride out the Arab oil embargo much better than its competitors.

Applying scenario analysis to develop management strategies requires creative thinking. Multiple scenarios for a world 10, 20, or 30 years into the future are imagined, and strategic courses of action required today to survive and prosper in those futures are explored through backcasting. By identifying common factors believed to be critical in multiple imagined scenarios and incorporating them into corporate strategies and business plans, companies can enhance their resilience to unexpected turns of events. The purpose of scenario planning is to use one’s imagination to learn from the future about how best to prepare for any uncertainties.

As the global economy shifts to multistakeholder capitalism, businesses and the financial sector need to embrace policies to not only ensure their own sustainability in the face of an intensifying climate crisis but also offer solutions to slow down and reverse climate change. Political leaders and government officials are not the only ones engaged in ensuring environmental and social well-being; as long as natural and social capital are being utilized to undertake economic activity, private companies are just as responsible. Of equal importance is the role of financial institutions in promoting energy and other innovations through capital flows so that the world can transition quickly and smoothly to a low-carbon economy.

The temptation among private companies to regard the TCFD Recommendations as one more international movement for onerous nonfinancial disclosures is understandable. But their real aim is to enable management to readily adapt to an uncertain future and to strengthen strategic resilience. Undertaking scenario analysis may be costly in terms of money and personnel, but it can confer far greater benefits, enabling companies to strengthen their corporate strategies and maintain long-term value. It can also lead to innovations that mitigate climate change and create additional value. Disclosures that demonstrate management’s climate-related initiatives and strategies, moreover, will facilitate the flow of funds to truly resilient businesses capable of sustained value creation, thus ensuring a healthy financial system and investment chain, as well as the stable growth of the financial market.