A distinguishing feature of the coronavirus shock has been its disparate impacts on different sectors of the economy. Senior Fellow Hideo Hayakawa discusses the likelihood of a multi-paced recovery and its implications for Japan’s economic outlook.

* * *

In Japan, as in most of the world, the COVID-19 pandemic triggered an abrupt economic contraction in the early spring of 2020. But the Japanese economy is believed to have entered a recovery phase after bottoming out in May, an assessment echoed by the Short-term Economic Survey of Enterprises in Japan, or Tankan, released by the Bank of Japan in October.[1] The question now is how quickly the economy is likely to recover, and the answer, as I argue below, depends very much on which sector one chooses to emphasize.

General Outlook

In the April–July quarter, Japan experienced a quarter-to-quarter drop of 28.1% in real gross domestic product, the worst quarterly contraction since World War II. But personal consumption, which accounts for more than half of Japan’s GDP, rebounded sharply in the July–September quarter. The government lifted the national state of emergency in June, which is also when many taxpayers received their stimulus payments. With restaurants and department stores reopening and cash on hand, conditions were ideal for a release of pent-up demand (or “revenge buying” in the current vernacular).

The surge fueled hopes for a robust recovery, but it was not to be. The epidemic’s spread accelerated again during the summer months, sending consumers scurrying back home and dampening consumption. Translated into quarterly GDP figures, these trends would be expected to yield a steep jump for the July–September period, followed by more modest growth in the October–December quarter. In the September ESP Forecast, compiled by the Japan Center for Economic Research, Japan’s economic forecasters predicted an annualized growth rate of 14.1% for the July–September quarter, falling to 4.5% in October–December and below 3% thereafter. In terms of annual growth, the consensus forecast estimates a dismal −6.1% in fiscal 2020 (ending in March 2021) and a modest 3.4% expansion in fiscal year 2021, followed by a lackluster 1.3% for fiscal 2022. If this outlook is accurate, it will be at least 2024 before Japan’s real GDP surpasses its previous peak (2019).

In short, if we define the end of the coronavirus recession as the point at which GDP overtakes the pre-pandemic peak, then we are looking at a decidedly slow five-year convalescence (even assuming no additional shocks). To be sure, it took five years for Japan’s GDP to return to its previous peak after the financial crisis of 2008, but in that case the recovery was hindered by multiple setbacks, including the 2011 Tohoku tsunami, the European debt crisis, and the yen’s extreme appreciation against the dollar.

Outlook by Sector

I agree with the consensus forecast on the whole, but I would caution that the pace of recovery is likely to differ significantly from sector to sector. In the following, I would like to consider the outlook for the digital, manufacturing, and (conventional) service sectors separately and consider some of the implications of a multi-speed recovery.

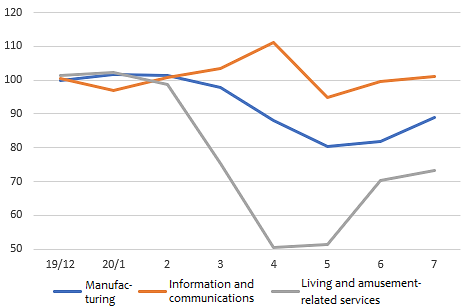

The digital economy, as one might suspect, is best positioned for a rapid recovery from the current recession, if only because it experienced such a minor downturn to begin with. In addition to being largely immune from the effects of shutdowns and the fear of infection, the digital economy benefited from a surge in demand created by the expansion of telework, online consumption, and other remote alternatives to personal interaction. According to the Indices of Tertiary Industry Activity, released by the Ministry of Economy, Trade, and Industry, the information and communications industry saw almost no net drop in activity last spring, and the software industry experienced an upturn.[2]

Figure 1. Indices of Industrial Activity by Sector (Oct.–Dec. 2019 = 100)

Sources: METI, Indices of Industrial Production and Indices of Tertiary Industry Activity.

These figures, moreover, fail to capture the full extent of activity in the digital sector. The recent explosion in telework shows up an increase in software licensing fees and sales of computers and peripherals (the latter falling under the category of goods, not information services), but the statistics tell us almost nothing about the value generated by telework itself. The same applies to remote learning, which accounts for the bulk of university instruction even now, after most workers have returned to the office. Economists, including Erik Brynjolfsson and Andrew McAfee, have been complaining for some time that official statistics ignore much of the economic activity taking place in cyberspace, and it seems to me that shifts in behavior triggered by the pandemic have accentuated this problem.

On the other end of the spectrum, services industries that rely on face-to-face contact, such as the restaurant, hospitality, recreation, and entertainment sectors, are facing an uphill battle. In April and May, METI’s Indices of Tertiary Industry Activity registered a precipitous drop in the category of “living and amusement-related services,” which encompasses the aforementioned sectors. Moreover, activity in that category remained far below pre-pandemic levels through June (see Figure 1), at a time when department store sales and automobile purchases were booming.

Tourism and dining out are expected to pick up—with a boost from the government’s “Go To” campaign[3]—with the further relaxation of local restrictions on business hours and activities. But if Japan should experience another resurgence of the coronavirus or a second wave similar to that currently menacing Europe, the government will be obliged to step in with strict social distancing measures, and even if businesses stay open, consumers are bound to stay away out of concern for their own health.

Generally speaking, the Japanese people have taken the threat of COVID-19 very seriously. Some observers have criticized their caution as excessive in view of the low rates of infection and especially mortality in Japan as compared with Europe or the Americas. But given the large share of elderly individuals in the population and the general Japanese tendency toward risk-averse behavior, we need to accept that it will take some time for high-contact services to recover in Japan.

Manufacturing and export businesses fall somewhere in the middle in terms of the pandemic’s impact and the likely pace of recovery. Exports and industrial output were expected to recover slowly after a steep drop in April and May, but so far performance has exceeded the forecasts. For example, month-on-month growth in real exports was a robust 7.7% in July and 6.5% in August. Industrial output, likewise, surged in July, by 8.7%, and while expansion slowed to 1.7% in August, METI’s Production Forecast Indices anticipate 5.7% growth in September and another 2.9% increase in October. Granted, these indices often err on the high side, but if they turn out to be on the mark, it will mean that fall output will have already returned to pre-pandemic levels.

Globally, a relatively quick resurgence in demand for goods would be good news for Japan’s export industries. Japan’s export performance naturally hinges on economic conditions in the importing countries, and the latest GDP forecasts seem to signal a sluggish recovery in the West. But those forecasts are heavily influenced by the outlook in the services sector, which accounts for such a large portion of the economy. Just as the demand for manufactured goods has recovered fairly quickly in Japan, it seems possible that global trade in goods will pick up faster than the GDP estimates suggest.

Implications of a Multi-Speed Recovery

The implications of a staggered recovery are significant. One is that a country’s rate of recovery will depend not only on the impact of the epidemic but also on that country’s industrial structure. This suggests that the economy best positioned for a swift and strong recovery is, ironically, China—where the pandemic began. In addition to having moved quickly to control the epidemic with strict lockdowns and sophisticated tracking and surveillance technology, China is strong in both the manufacturing and digital sectors. It is probably unrealistic, though, to hope that China will experience a growth spurt comparable to that which helped pull the entire world out of the Great Recession; Beijing has been relatively circumspect about using public investment to stimulate the coronavirus-hit economy, recognizing that the 4-trillion-yuan stimulus plan it adopted to counter the effects of the 2008 financial crisis fueled a massive asset bubble. Even so, China is the only country among the world’s major economies that clearly entered the recovery phase in the April–June quarter. Despite concerns about escalating friction with the United States, China has a decided edge in the global post-pandemic recovery.

The United States, by contrast, continues to wrestle with high rates of infection, and while its world-leading digital information and communications industry is certainly an asset, a particularly heavy dependence on the services sector could hobble the recovery. Among the industrially advanced countries, Germany and Japan stand out both for their comparatively robust manufacturing sectors and for their relative success in containing the coronavirus. But they also lag far behind the United States and China when it comes to digitalization of the economy. In Japan and most of the West, the slow growth that characterized the decade following the Great Recession seems bound to continue.[4] Italy and Spain, which were hard hit by COVID-19 deaths in the spring, may face the highest hurdles to recovery, given their relatively undeveloped digital and manufacturing sectors and their heavy dependence on tourism. Long-term stagnation is a particular concern for Italy, whose economy never did regain the ground it lost in the Great Depression.

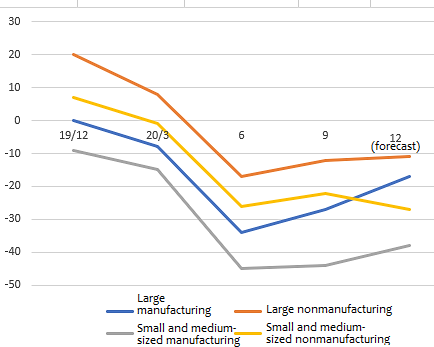

The second implication of the multi-speed recovery is the danger of over-reliance on standard economic indicators, such as industrial output and the Tankan large manufacturers index, when assessing the state of the recovering economy. Economists have traditionally placed heavy emphasis on manufacturing indicators, and many continue to do so despite the fact that manufacturing’s share of total economic output has dropped to about 20%. The Japanese economy’s reliance on manufacturing activities is clear from the frequency with which the shift between expansion and contraction phases coincides precisely with the start of an uptrend or downtrend in exports. If indeed the impact of the coronavirus differs sharply between the services and manufacturing sectors, as seems likely, then a narrow focus on manufacturing trends could cause the government to overestimate the strength of the recovery. In fact, big manufacturers’ assessment of business trends, as seen in the Tankan large manufacturers index—the most closely watched of the BOJ’s economic indices—has risen considerably faster than the other three indices compiled from the Tankan “judgment survey” (Figure 2). But because of the disparity between goods and services, the economy as a whole is recovering at a much slower pace.

Figure 2. Business Conditions Diffusion Indices (aggregated from the results of the BOJ Tankan judgment survey)

In an earlier article analyzing the surprising strength of the stock market despite the coronavirus downturn, I emphasized the role of tech stocks. At this point, I think we should consider another factor, namely, the biased composition of companies listed on the stock exchange. In Japan, almost all large manufacturing firms are publicly listed corporations. By contrast, the vast majority of businesses in the “face-to-face sector” are small unlisted companies. Given that bias, it seems highly probable that the stock market gives an overly optimistic picture of the current recovery.

The third major implication of a multi-speed recovery pertains to employment. While low by international standards, Japan’s unemployment rate (which excludes those who have been temporarily laid off) has been rising slowly since the pandemic struck, hitting 3.0% in August. At the same time, the ratio of job offfers to applicants has dropped from around 1.6 to about 1.0. Most experts doubt that unemployment will surpass 5%, as it did during the Great Recession, given that Japan’s population has entered a decline, creating labor shortages in some sectors. Instead, they say, the influx of women and seniors into the labor force—a trend actively encouraged in recent years—will fall off as job openings dwindle.

However, this viewpoint ignores the disproportionate impact of the coronavirus on the face-to-face sector, which is labor-intensive. According the Japanese government’s Labor Force Survey, the two categories of “accommodations, eating, and drinking services” and “living-related, personal, and amusement services” together account for around 10% of the labor force, and the share rises to 22% when medical, healthcare, and welfare services are added in—as compared with 15% for the entire manufacturing sector.[5] Given the large number of people working for businesses heavily impacted by the coronavirus, both in Japan and around the world, there is good reason to fear a “jobless recovery.”

We must also be prepared for the likelihood that some businesses will never fully recover, either because the market (notably inbound tourism) continues to languish long after the domestic health crisis is past, or because their business model is no longer viable. In such cases, it is essential that the government shift the focus of its response from emergency loans and subsidies designed to prop up businesses to retraining and recurrent-education programs oriented to protecting lives while building new capacity.

[1] In addition, in October the government upgraded its assessment of the economy based on the Cabinet Office’s coincident index of business conditions from “worsening” to “bottoming out.”

[2] In July, the activity index for the information and communications industry as a whole fell just 0.7%. Within that category, software rose 2.1%, with software products registering a jump of 24.7%.

[3] The “Go To” campaign is a plan to boost demand in the restaurant, hospitality, and travel industries by offering consumers government-subsidized discounts and vouchers. Where tourism is concerned, however, some have argued that it would be a better use of government funds to subsidize the industry directly, particularly during the off-season.

[4] For a discussion of the possible impact of the pandemic on Japan’s potential growth rate, see my article “Japan’s Potential Growth Rate and the Post-Pandemic Outlook.”

[5] The disparity is particularly pronounced for women, who account for 35% of employees in the face-to-face (and health-related) sectors and just over 10% of manufacturing.

-

-

- SENIOR FELLOW

- Hideo Hayakawa

- Hideo Hayakawa

- Areas of Expertise

-

- Japanese economy

- monetary and fiscal policy

- economic thought

-

Featured Content

-

Funding the Policies to Boost Japan’s Birthrate

Funding the Policies to Boost Japan’s Birthrate

-

CSR in Japan: Unique Features and Recent Trends

CSR in Japan: Unique Features and Recent Trends

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

-

Funa Zushi

Funa Zushi

-

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform