- Article

- Tax & Social Security Reform

A Consumption Tax Cut Would Undermine Fiscal Sustainability: Tax & Social Security Reform Unit’s Urgent Appeal for Discipline amid Pandemic

July 2, 2020

While acknowledging the need for aggressive fiscal measures to revive the coronavirus-stricken economy, the members of the Foundation’s Tax & Social Security Reform Unit argue strongly against a consumption-tax cut in this joint appeal.

* * *

The economic fallout from the COVID-19 pandemic is assuming unprecedented proportions, both globally and nationally, and governments around the world are mobilizing forceful fiscal and monetary measures to mitigate the damage. At the same time, there is growing alarm over signs that these efforts are eroding fiscal discipline. In Japan, there are continuing calls for a cut in the consumption tax, which helps finance our social security system, including healthcare, nursing care, and old-age pensions.

The members of the Foundation’s Tax & Social Security Reform Unit oppose a reduction in the consumption-tax rate on the grounds that such a cut is an inefficient, costly form of relief that could have serious repercussions for the sustainability of social security. Indeed, given Japan’s current fiscal situation and its rapidly aging population, we believe the long-term consequences could be disastrous.

Erosion of Fiscal Discipline

The National Diet passed a supplementary budget for fiscal 2020 on April 30, and a second supplementary budget, approved by the cabinet of Prime Minister Shinzo Abe on May 27, is currently before the legislature. Together, they amount to more than ¥50 trillion, almost all of which will have to be paid for by government bonds. In fiscal 2020 alone, the budget deficit is expected to reach more than 10% of gross domestic product, and the government’s total bond issuance, including refunding bonds, will surpass ¥250 trillion.

There is no question that an emergency like the COVID-19 epidemic calls for a major outlay of public funds to rescue the economy and sustain people’s livelihoods. But even when pursuing an expansionary fiscal policy, a basic level of discipline must be maintained. Unlike some countries, Japan has not prepared itself for an emergency like this by budgeting responsibly during ordinary times. Consequently, it is already grappling with a national debt amounting to well over 200% of GDP, with that ratio poised to rise sharply as a result of the coronavirus crisis. Moreover, the nation is likely to face other emergencies in the years ahead. There is a high probability that the Tokyo area, the southern coast of Honshu, or both regions will be hit by a disastrous earthquake within the next few decades. Damaging typhoons and other extreme weather events are on the rise. We must build the fiscal resilience to manage multiple risks.

Unfortunately, the two massive supplementary budgets in response to the coronavirus have already breached the constraints of fiscal discipline. The prevailing view is that this is no time to be thinking about fiscal health. But the emergency should not become an excuse for abandoning the long-term goal of fiscal retrenchment. The novel coronavirus is not the only crisis facing Japan. The costs of pension and healthcare benefits are poised to skyrocket as the graying of Japanese society continues. Under the circumstances, further deterioration of government finances could threaten the sustainability of our social security system. We must not let the current crisis plant the seeds of a social security crisis.

To preserve fiscal discipline and protect social security, it is essential that we prevent emergency expenditures from turning into permanent spending programs. The coronavirus-response budget must be cordoned off from the general account budget and the government’s roadmap for fiscal reconstruction.

To this end, we call for the creation of a “coronavirus response special account” comparable to the special account for reconstruction established in the wake of the Tohoku earthquake and tsunami of 2011. The coronavirus account should be placed under unified management and oversight, and time limits should be imposed on all expenditure items with the exception of debt repayment.

In addition, to ensure that the burden is not shifted to future generations, the government should begin considering a new low-rate tax or surtax to finance long-term repayment of the coronavirus-response debt (over 10 or 20 years, for example) once economic activity has returned to normal. After the Great East Japan Earthquake, the government issued special reconstruction bonds to raise funds for recovery and reconstruction and secured revenues for repayment through a special 25-year 2.1% surtax on the national income tax and a flat 10-year ¥1,000 surtax on the individual inhabitant (local income) tax. We need to have a deeper discussion about options for paying off the coronavirus debt and begin to make the necessary preparations.

Drawbacks of a Consumption-Tax Cut

For months now, Japanese politicians spanning the ideological spectrum have been agitating for a cut in Japan’s national consumption tax in response to the coronavirus crisis. Such calls are bound to grow louder in the wake of the June 3 decision by Germany’s coalition government to reduce the standard rate of the value-added tax from 19% to 16% (and the reduced rate from 7% to 5%) for a period of six months, starting July 1, as part of a stimulus package to reboot the economy.

While we understand the need to consider a wide range of policy options to deal with the economic crisis, we do not believe that a cut in the consumption-tax rate is a sensible option for Japan. Our reasoning is as follows.

A Vital Resource

First, the national consumption tax is an earmarked tax levied for the express purpose of financing social security programs. All revenues from the consumption tax are dedicated to social security. Under the government’s policy to develop “a social security system oriented to all generations,” this encompasses not only healthcare, nursing care, and pension benefits for our aging society but also free daycare and preschool.

In short, the consumption tax supports many of the essential services on which the Japanese people depend. The consumption tax is also used to pay down the national debt and shore up government finances during ordinary times, thereby contributing to the long-term sustainability of the social security system. Any reduction in the consumption-tax rate would be at odds with the nation’s medium- and long-term policies and could have grave repercussions farther down the road.

From the beginning, a portion of the revenues from the consumption-tax increase agreed in 2012 was earmarked to boost the government’s contribution to the Basic Pension. If some or all of that revenue disappeared, the government’s contribution (and thus pension benefits) would need to be reduced accordingly. Drawing on the pension fund’s asset reserves would only hasten their depletion.

The ruling party promised the electorate that revenues from the consumption-tax increase would go to support old-age pension benefits and free early-childhood education. To rescind the increase without halting those expenditures would make a mockery of that pledge. To compensate for the loss of revenue, the government would doubtless be obliged to hike social insurance premiums and healthcare copayments. High pension and health insurance contributions already impose a heavy burden on the working-age population and have a negative impact on employment.

Furthermore, if the effects of a consumption-tax cut are to be fully realized, the decrease must be reflected in the fees charged by healthcare providers. However, this is extremely difficult to arrange. Because services provided under the national health and long-term care insurance systems are exempt from the consumption tax, healthcare facilities are unable to claim deductions to recoup the costs the tax incurs when they purchase supplies and equipment. Instead, the government has used complicated formulas to adjust the amount it reimburses providers for various health service fees. But the formula has changed over the years, and untangling it would be virtually impossible. Under the circumstances, a cut in the consumption tax would cause unnecessary confusion in the healthcare system.

A Delayed-Action Stimulus

Another major drawback to a tax cut is the amount of time it would take to be implemented and provide the intended relief. A change in the tax rate involves painstaking and time-consuming drafting of legislation, including provisions covering transitional measures. One-time cash subsidies, by contrast, require only a supplementary budget, which can be drawn up quickly without amending any laws.

Moreover, with the current regular session of the Diet scheduled to end on June 18, there is barely enough time to deliberate and pass a second supplementary budget, let alone an amended Consumption Tax Act. In addition, businesses need time to adjust their accounting procedures, and government agencies need time to adjust the fees charged by public or regulated services, such as postage and taxi rates. All told, a tax cut would take months to implement.

Furthermore, if a consumption-tax cut were planned, households and businesses would doubtless do their best to delay purchases until the new rate came into effect, exacerbating economic instability.

Another issue is the time and political capital required to return the consumption tax to its current rate once it is lowered. The consumption tax took almost a decade to implement (in December 1988) at the original rate of 3% and was finally edged up to 5% in April 1997. It then took another 17 years to increase the rate to 8% in April 2014. The final increase, from 8% to 10%, took an additional 5 years, having been postponed twice before it was finally implemented in October 2019. Tax increases are unpopular, and the current 10% level has only been achieved at great political cost. If the government caves in to pressure and lowers the rate, the national debt will soar, and all that time, effort, and sacrifice will have been in vain. It could take years to restore the consumption tax to its current level.

A Cost-Ineffective Measure

A consumption-tax cut is a particularly costly and inefficient option for relieving the economic distress caused by the COVID-19 pandemic. The economic impacts of the epidemic have been very uneven. Higher income earners in the IT sector, regular salaried employees at big corporations, and civil servants appear to have suffered very little, at least as far as income is concerned. (The April 2020 Family Income and Expenditure Survey showed little year-on-year change overall). Instead of targeting assistance where it is most needed, a consumption-tax cut would benefit even those who have made out well during the crisis.

Consumption taxes are typically viewed as regressive, since they take a proportionately bigger chunk out of the earnings of low-income households. But the biggest beneficiaries of the cuts being proposed would be high-income households that spend a larger portion of their income on big-ticket items like cars and condos. In other words, a consumption-tax cut is a tax break for the wealthy, as we show in the table below. This seems like a waste of resources. Surely it would make more sense to target government spending to those who are having trouble making ends meet.

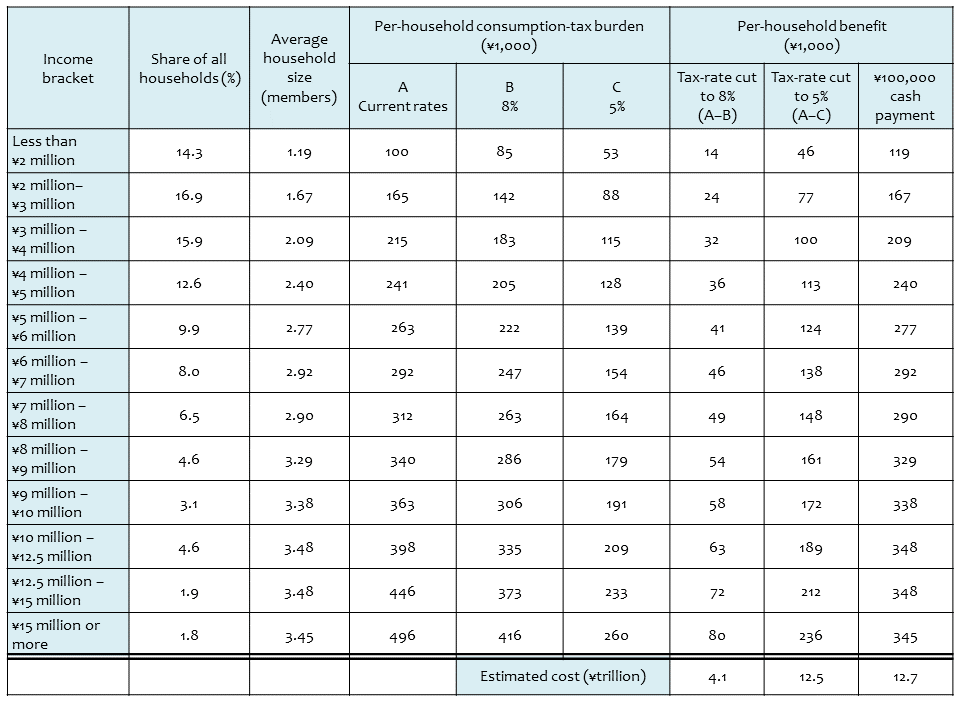

Average Savings from Consumption-Tax Cuts by Household Income

Source: Estimated values calculated by Takero Doi based on figures published in the 2018 Annual Report on the Family Income and Expenditure Survey (Statistics Bureau of Japan, Ministry of Internal Affairs and Communications).

The estimates tabulated here support our assertion that a consumption-tax cut would confer the most benefits on high-income households. (For a detailed explanation of the calculations, see Note on Methodology, below.) Column A shows the estimated per-household annual consumption-tax burden by income bracket (based on 2018 consumption levels), under the tax rates that went into effect in October 2019 (10% standard rate, 8% reduced rate, and 0% for exempt items). Column B shows the burden that would result if the rate were reduced to a flat 8% for all taxable items. Column C posits a flat 5% rate on all taxable items.

The last three columns in the table (right-hand side) show the estimated average benefit to households in each bracket from each of three fiscal measures: a cut in the consumption tax to 8% (A–B), a reduction to 5% (A–C), and the uniform one-time “special cash payment” of ¥100,000 per person included in the first supplementary budget.

Under the 5% option (A–C), households earning less than ¥2 million per year would save approximately ¥46,000 a year on average. For those in the ¥4 million–¥5 million bracket, the average savings would be ¥113,000. Those earning ¥15 million or more would get a ¥236,000 windfall on average. Meanwhile, cutting the consumption tax to 5% would cost the government an estimated ¥12.5 trillion in annual tax revenues. This is close to the total cost of the uniform one-time special cash payment. Yet the ¥100,000 cash payment has a bigger per-household impact, particularly for those in the lowest income brackets. From a cost-benefit standpoint, even an across-the-board cash handout makes more sense than a consumption-tax cut.

Japan Is Not Germany

Why, then, did Germany decide to cut its value-added tax rates? The difference between Japan and Germany is that Germany had something to “give back” to its people after running a budget surplus for six straight years.

Having raised its VAT rate to 19% in 2007, Germany maintained that rate even after the global financial crisis hit, causing the economy to shrink by 5.6% in real terms. In 2009, in the face of a growing budget deficit, the government amended the constitution to include a “debt brake” provision that drastically limited the structural federal deficit, beginning in 2016. Aware that it would be forced to raise taxes if it failed to rein in spending, the government cut back on healthcare costs and other expenditures. As a result, the federal government began posting a budget surplus in 2014. (The balance of the federal and Länder budgets combined has been in the black since 2012.)

Even before the coronavirus hit, Germany’s coalition government had been actively debating measures for returning part of the surplus to the nation; Chancellor Angela Merkel’s Christian Democratic Union favored cuts in corporate and individual income taxes. In response to the crisis, the coalition ultimately agreed on a temporary cut in the VAT. But even after the cut, the standard rate will be 16%, substantially higher than Japan’s 10%.

The Japanese government, by contrast, effectively abandoned its initial target of achieving a primary surplus by 2025. Its fiscal policy appears to have been driven by wishful thinking, the hope that economic growth would reduce the debt-to-GDP ratio even without active efforts to reduce deficit spending. In fact, we have seen no significant reduction in the debt-to-GDP ratio over the past five years. This dithering on fiscal reconstruction has cost us dearly. The coronavirus crisis has struck while Japan’s government finances are still precarious.

Despite this dire situation, the Japanese government has put together one of the biggest relief packages of any government in the Group of Seven. It has allocated funds for a uniform one-time ¥100,000 cash payment to all residents who apply for it, regardless of their means. The total bill for this handout is estimated to be roughly equal to the revenue from a 5% consumption tax. The inevitable result will be a sharp deterioration in the government’s financial position.

To abandon fiscal discipline for the sake of an aggressive fiscal response is neither wise nor practical. The example of Germany teaches us that those who exercise fiscal discipline in ordinary times are rewarded with the capacity to launch an aggressive fiscal response in times of crisis. The Japanese government, by contrast, has faltered repeatedly in the face of deep-seated political resistance to fiscal discipline, including necessary consumption-tax increases. The consumption tax finances basic government expenditures, including those that support social security. A tax cut at this time would undermine the social security system.

Instead of an across-the-board tax cut, the Japanese government should work on targeting cash payments and other forms of relief where they will do the most good—that is, to the households and businesses that are truly in need. In addition, it should follow Germany’s example by clarifying in advance how it will repay the debt generated by economic relief measures taken in response to the coronavirus crisis.

As we have seen, a consumption-tax cut would be a costly and inefficient means of providing short-term relief in response to the coronavirus emergency. It would also undermine fiscal discipline and compromise the sustainability of the social security system. Japan is in no position to do either.

Note on Methodology: Estimation of Tax Burden and Savings

The figures in the table are the estimated averages for households in each income bracket, calculated on the basis of figures compiled by the Japanese government in its 2018 Annual Report on the Family Income and Expenditure Survey, published by the Statistics Bureau. The figures represent a weighted average of estimates for single-person households and larger households. The reason for using consumption figures from 2018 is that it was the last year when a uniform rate of 8% applied to all items subject to the consumption tax, making it easier to gauge the tax rate’s impact. To calculate the consumption-tax burden, tax-exempt items were subtracted from annual household expenditures, and the rest were broken down into standard-rate items and reduced-rate items. The consumption-tax component of those expenditures was then calculated to arrive at the estimated annual tax burden in yen.

One reason for the difference between the all-household total for the special cash payment and that for the consumption-tax cut is that tax-burden estimates here do not include (1) the consumption tax on home purchases, and (2) taxes that the operators of tax-exempt businesses and public services paid on business-related purchases but did not levy on consumers. However, most households would not directly benefit from the reduction of this tax burden.

-

-

- RESEARCH DIRECTOR

- Shigeki Morinobu

- Shigeki Morinobu

- Areas of Expertise

-

- Tax and fiscal policy

- local finances

- Research Program

-

- The History of Japan’s Consumption Tax: An Archive of Key Events and Documents ( –2021)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan (2021–2022)

- Digitalization of the Economy and International Taxation(-2024)

- Assessing the Integrated Reform of Tax and Social Security Systems in Japan 2

-

-

-

- RESEARCH DIRECTOR

- Takero Doi

- Takero Doi

- Areas of Expertise

-

- Public economics

- fiscal policy

- taxation

- social security

- income distribution

-

-

-

- Counselor / Chief Senior Economist, Japan Research Institute

- Kazuhiko Nishizawa

- Kazuhiko Nishizawa

-

-

-

- RESEARCH DIRECTOR

- Kazumasa Oguro

- Kazumasa Oguro

- Areas of Expertise

-

- Public finance

- social security

- public economics

- generational gap

- population problems

- Research Program

-

-

-

- Professor, Institute of Economic Research, Hitotsubashi University

- Takashi Oshio

- Takashi Oshio

-

-

-

- RESEARCH DIRECTOR

- Motohiro Sato

- Motohiro Sato

- Areas of Expertise

-

- Local public finance

- Optimal taxation theory, tax reform

- Social security, health economics

-

-

-

- Professor Emeritus, Hitotsubashi University

- Eiji Tajika

- Eiji Tajika

-

Featured Content

-

Funding the Policies to Boost Japan’s Birthrate

Funding the Policies to Boost Japan’s Birthrate

-

CSR in Japan: Unique Features and Recent Trends

CSR in Japan: Unique Features and Recent Trends

-

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

Partnering with Business to End Poverty: Lessons from NGO Gawad Kalinga

-

Is the Digital Transformation of Education a Realistic, Sensible Goal?

Is the Digital Transformation of Education a Realistic, Sensible Goal?

-

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform

Making Work Pay for Japanese Women: Toward a Smarter Approach to Tax and Social Security Reform